Back

August 11, 2025

Crypto ethos was once an ethos of permissionlessness, a desire to fall outside the system, and an underlying theme of anarchism, much like the kid in his early teens looking to stand out, and be different. However, as kids grow up, so did crypto, and with that came an understanding of the benefits of conforming. Greater capital, greater profits, and an opportunity to move from slacks, T-shirts, and memes to Brooks Brothers Suits and Rolex watches (the memes stay intact, of course).

As with early adults who do just about anything to land that shiny Investment Banking/ Consulting job, crypto is now bending over backwards to engineer its innovations to fit traditional finance legislations. While this is driven partly by the desire to conform, the other reason for this is that it is finally a serious money making business - and an alternative set of instruments where the spreads are still wide, liquidity still limited to a fraction of the big banks’ balance sheets, and an opportunity to employ the Wall Street Weapons of Mass Destruction - HFT systems, moving option prices via manipulation of underlying small cap indices (Jane Street, looking at you), and short squeezes for passive yields. A lot of this has already materialized- however, to increase the money that flows into this system, innovators need to find ways to plug in crypto perps, options, and unregulated venues to conform to regulations across the world.

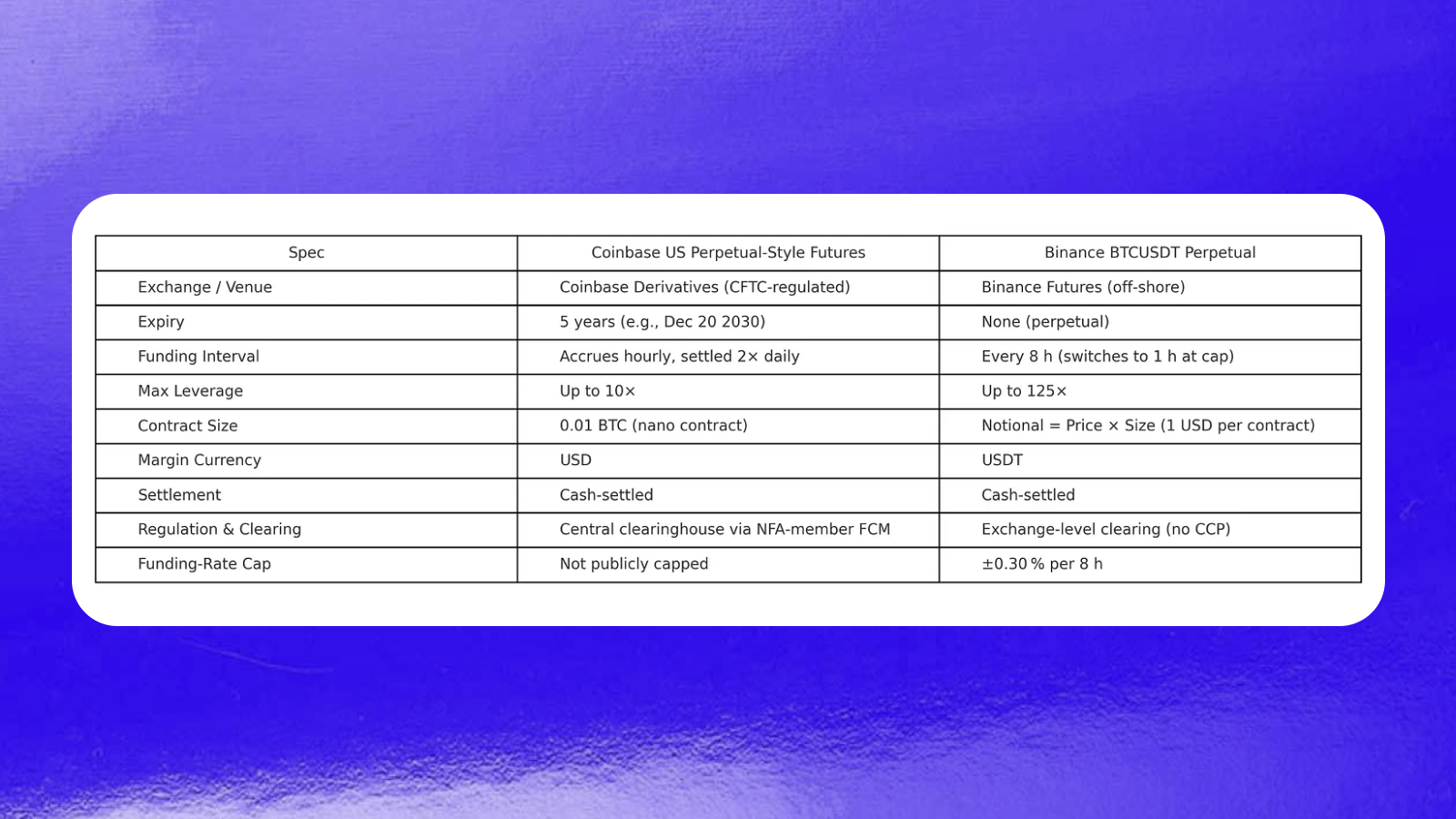

This is evident with the most recent announcement by Coinbase to launch CFTC regulated perpetual futures. In its unregulated version, perpetual futures are futures with no expiry, and a 4- 8 hour settlement via funding rate transfer between longs and shorts based on the perp price difference to the asset price, with infinite leverage.

In its regulated form, for all intents and purposes, Coinbase’s US perpetual style futures have benefits very similar to the unregulated parts, but with mechanisms that make it kosher for the CFTC to regulate. Instead of no expiry, these perps expire every five years. The funding intervals are changed to 12 hours from 8 hours to make a middle way between the daily settled futures of trad-fi vs the 8 hour settled perps of Binance. This change in funding intervals also allows for a Central Clearing house to participate in the 24 hour crypto market, which was previously not possible on CME cash-settled BTC or ETH futures, by virtue of 5pm settlements on working days.

The above is an excellent study in what is set to happen across capital infrastructure- lending, borrowing, collateralization, derivative treatments, and probably even payments.

The thesis here is that the net new innovations of crypto will become modifications to trad fi versions of these contracts. This is partly due to how regulations are designed and operated. In conversation with regulatory bodies across different countries including India, the UAE and others, what was a common line of thinking was that newer technologies need to ideally fit into existing buckets, and to the extent possible, will be made to do so.

From a regulator’s and a bank’s perspective, this is not novel. It makes sense. The reason is that the underlying economic activity of most crypto-related activities is centred around three things that are common to all monetary systems:

Either way, the complex mechanics of DeFi systems are not new, but extremely similar to the financial primitives of the traditional finance world - hence it makes sense to regulate them that way.

As a result and a consequence, what is projected to happen in the system is that the mainstream adoption of crypto technologies and ecosystems will only happen when these square pegs fit in the round holes of trad-fi. You have a perp? Make it look like a future. You wanna borrow against this exotic currency - make it look like a tier 1 equity. If you wanna trade baskets, make them trade like forex- bring in ECNs and compliant prime brokers- maybe even exchanges.

The following sections will highlight the art of possible in different parts of the financial ecosystem, and how we already see momentum in the bridges that will eventually solidify.

Coinbase’s five-year “perps” are only the opening act. CME - which used to look like the button-down chaperone at a rave - is suddenly the fastest-growing crypto derivatives venue. Average daily crypto volume jumped from ≈10 K contracts in Q3 2023 to 198 K in Q1 2025 - a 19× move in six quarters.

Why the rush? Two words: margin offsets. Once a contract is cleared through a real CCP, delta hedges and Treasury collateral start netting against the rest of the house book. That’s catnip for bank desks who have been stuck warehousing basis risk on offshore venues. However, there are still a few barriers to the growth of this play into its maturity:

What’s next? Expect CME to list basis-style crypto IRS that let dealers trade funding-rate curves the way they trade SOFR vs. Fed funds. This is already materializing on a private basis with various vault operator/ vault aggregator startups with enough TVL/ lending relationships with large asset allocators creating these curves both for their own use as well as for public consumption.

Loans against crypto collateral remain the regulatory equivalent of smoking in a jet-fuel depot. Basel’s 1,250 % risk weight on “Group 2” crypto makes a fully-collateralised BTC loan consume as much capital as an unsecured LBO.

Enter the ETF work-around: treat spot-BTC ETFs as plain-vanilla equity. Under the standardised approach that’s a 250–400 % risk weight—painful, but merely borderline stupid rather than existentially so. Banks like JPM are already piloting UHNW lending lines secured by ETF shares, precisely because auditors will sign off on the look-through.

However, this is not where this ends- the risk weights can further be trimmed through rehypothecation of the ETF shares into a repo. The way this works is - take the example of JPM’s UHNW client lending against BTC ETF collateral. The bank lends at 60% LTV, let’s assume - fairly conservative and typical of a tier 1 equity collateral. As a part of the lending activity, the bank signs a standard securities lending or pledge agreement- which allows the bank to re-use the collateral.

The bank immediately then turns around and enters a tri-party repo with a money-market fund, by selling the same ETF shares to MMF for a minor discount on the position and agrees to repurchase them the next day, for a small overnight interest rate. As a result, the ETF shares, which are weighted at 250-400% risk weight are no longer on the bank’s balance sheet, but on the Money Market Fund’s balance sheet. Instead, what the bank is dealing in terms of risk now is the counterparty risk with the MMF, a mere 10% risk weight, making this incredibly capital efficient - earning a yield from both the bank’s borrower - the hedge fund, as well as the yield that the money market fund pays the bank for the overnight collateral it provides the fund.

Over the last year or so, the in thing for a lot of new crypto startups has been marketing multi-basket indices. Basket products are the crypto equivalent of traditional ETFs: rather than individually picking and trading multiple tokens, investors can buy a single instrument that tracks a group of assets.

This concept is already gaining traction. Cboe’s mini-Bitcoin index futures show U.S. regulators are comfortable approving crypto-linked indices when they clear via established clearinghouses. Meanwhile, Europe’s recent MiCA regulation, effective January 2025, enables companies to launch regulated crypto-based index products across all EU member states without needing separate approvals from each country. Similarly, the U.S. OCC Letter 1183 has streamlined approvals for banks to offer tokenised baskets, significantly reducing procedural complexity.

Banks are enthusiastic because these baskets offer clear advantages, or because they can capture fat management fees. A single crypto-index product simplifies their risk management, reducing complexity and costs. Additionally, clearing basket products through familiar clearinghouses lets banks combine margin requirements across products, freeing up capital. Clients benefit too - large investors often prefer diversified exposure rather than betting on individual tokens.

In the near future, this is likely to evolve into sector-specific baskets around lending, borrowing, restaking, L1 ecosystems, stablecoins, trading strategies- mimicking the themes that newer vault providers today are looking at.

The logical conclusion of this evolution in regulatory affairs and the forced mounting of crypto-railguns on to trad-fi starships, albeit with improper mounts, has implications for the industry’s builders and investors - specifically,